Blog

Special Report: Biotechnology Companies & Securities Class Action Litigation (2024)

Priya Cherian Huskins

Priya Cherian Huskins

Apr 02, 2025

Apr 02, 2025

In 2024, biotechnology companies were the second most targeted industry for securities class action litigation, according to the D&O Databox™, Woodruff Sawyer’s proprietary database of securities class action suits. The plaintiffs’ bar’s playbook is well-known: wait for some bad news, watch the stock price drop, look through previous company statements, and finally file suit alleging that these statements were fraudulently made.

The playbook is brutal, but judges in federal courts are far from naïve. This was on excellent display when looking at certain 2024 case dismissals.

In this article, I will provide some statistics for biotechnology litigation in 2024, examine some cases that took a hard look at scienter on the way to winning their motions to dismiss (as featured in a report just released by the law firm Sidley), and provide practical takeaways for directors and officers of life science companies.

Securities Class Action Litigation in the Biotech Industry

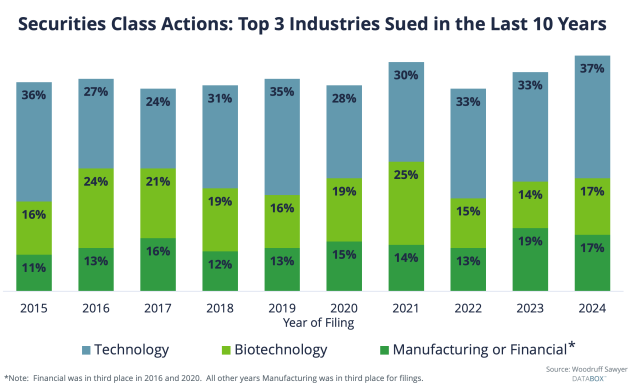

After technology companies, biotechnology companies are reliably among the most sued in any given year. The year 2024 was no exception, with biotech seeing 17% of filings—though it did tie with manufacturing last year (and actually came in third place in 2023).

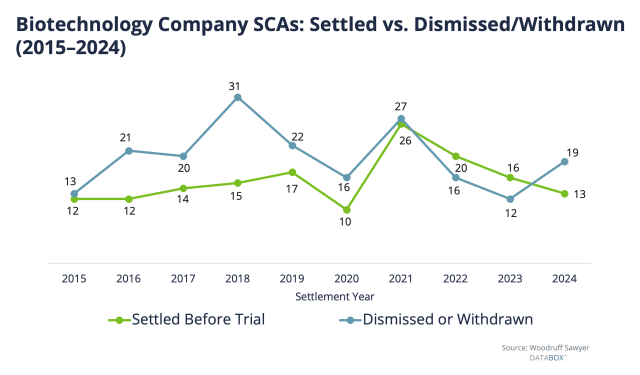

Plaintiffs do not limit themselves to “good” cases, as demonstrated by the fact that so many cases are won on a motion to dismiss or withdrawal rather than end in a settlement (actual trials are very rare).

In other words, most years, there are more dismissals and withdrawals than settlements. (While that was actually not true in 2022 and 2023, it went back to being true in 2024.)

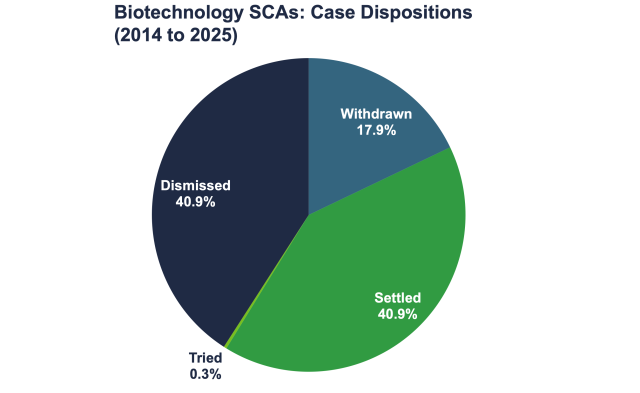

Here is another way to view case dispositions from 2015 to 2024, this time by percentages:

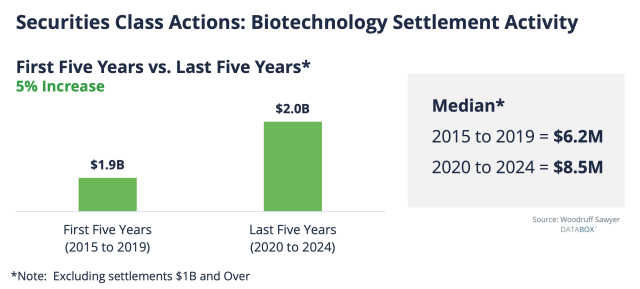

Settlement values, unfortunately, are trending upwards. This is something we discussed at length in Woodruff Sawyer’s D&O Databox 2024 Year-End Report.

Biotech company settlement dollars in the past five years have increased 5% in comparison to settlement dollars over the previous five years. The median settlement between 2020 and 2024 was $8.5 million.

However, there were much larger settlements as well, upwards of $400 million, as shown in the chart below.

| Top 3 Settlements in the Last 5 Years (2020 to 2024) | |||

| Entity | Settlement Year | Cash Settlement Account | Case Notes |

| Teva Pharmaceuticals Industries Ltd. | 2022 | $420M | Price-fixing, collusion inter-related with a large acquisition |

| Allergen plc | 2021 | $130M | Antitrust investigation of price collusion for certain generic drugs in which a dozen companies were being investigated by the DOJ |

| Alexion Pharmaceuticals, Inc. | 2023 | $125M | Fraudulent sales tactics to boost sales. SEC settlement of FCPA violations for $21M in 2020 |

Detailed Securities Class Action Case Analyses: The Sidley Report

Sidley’s 11th annual survey of Securities Class Actions in the Life Science Sector1 provides in-depth analyses of the appellate and district court decisions rendered in 2024.

As in past years, the report divides the world into cases related to drugs and devices at either the development stage or post-approval stage.

One of the most valuable parts of the Sidley report is its insight on how to consider disclosure broadly, particularly risk factors. The report also provides practical guidance, including for things like receiving a Form 483 notice.

Among the most interesting topics in this year’s report is the analysis of cases in which the court discussed and then dismissed Rule 10b-5 claims for lack of scienter.

As a reminder, the elements of a good Rule 10b-5 claim under the Securities Exchange Act of 1934 include2 material misrepresentation or omissions made with the intent to deceive, i.e., scienter.

Three cases discussed in the Sidley report, BioXcel, Revance, and AcelRx, are ones in which the court concluded that defendants may have been aware of facts that tended to undermine the defendants’ public statements, thereby supporting an inference of falsity.

However, because of the required scienter element of a 10b-5 claim, merely being wrong about something is not enough for the plaintiffs to establish liability.

Plaintiffs must also establish that the defendants acted with the intent to deceive, which is to say making a statement they believed to be untrue at the time they made it.

|

As the Sidley report summarizes so well: |

|

[Defendants] may be aware of problems with a product but still believe their optimistic statements about it are true—because they have confidence the problems can be addressed, even if others at the company believe otherwise. |

Also, the fact that a statement later turned out to be wrong does not mean the statement was fraudulent at the time it was made.

This was the animating nuance that caused the court in BioXcel to dismiss the case (with leave to amend) even though the plaintiffs’ allegations about the falsity of certain statements were sufficient.

In Revance, the company was wrong about the date it would obtain FDA approval, but plaintiffs failed to plead facts about the defendants’ state of mind.

In AcelRx, the fact that a confidential witness believed a statement at issue was false was not enough defeat the motion to dismiss since the plaintiffs failed to establish that defendants concurred with the witness that the statement was false. In all three cases, defendants won their motions to dismiss because plaintiffs failed to sufficiently plead scienter.

Takeaways

Disclosure for any public company is challenging. It is especially difficult for life sciences companies due to the complex issues they face daily.

Unfortunately, directors and officers of life sciences companies know that, even when they do their best, their disclosures will be challenged.

Of course, that is the job. Part of doing the job well is staying up to date on the nuances of how courts look at disclosure challenges.

Reviewing data like that in the Sidley report well before your company has an issue will go a long way to helping you navigate tricky disclosure challenges as they arise.

All of this also underscores the importance of strong D&O insurance. Public company self-insured retentions are high these days. As a result, you may well win your final motion to dismiss without exceeding your D&O insurance policy’s self-insured retention. If, however, you fail to win on a motion to dismiss, you will be glad for the protection that a properly sized D&O insurance policy can offer.

1 Woodruff Sawyer’s Biotechnology sector category includes pharmaceutical companies and excludes medical devices. Sidley’s Life Science report includes both pharmaceutical and medical device companies.

2 More completely, the elements of a Rule 10b-5 claim are a (1) material misrepresentation (or omissions), (2) made with an intent to deceive (scienter) (3) in connection with the purchase or sale of a security, (4) on which the plaintiff relied, (5) leading to economic loss that (6) was causally connected to the material misrepresentation (loss causation). Dura Pharmaceuticals, Inc. v. Broudo, 544 U.S. 226 (2005)

Author

Table of Contents