Blog

Medicare Guidance for Employers

Jeff Colby

Jeff Colby

Brandi Kyle

Brandi Kyle

Jan 24, 2024

Jan 24, 2024

More Americans are turning 65 than at any other time our country has ever known. We are now in the era of what is being called Peak 65, but rather than seeing a reduced workforce we’re finding more baby boomers opting to delay retirement. One result is an increased number of employees who are now navigating choosing between their employer sponsored medical benefits and Medicare.

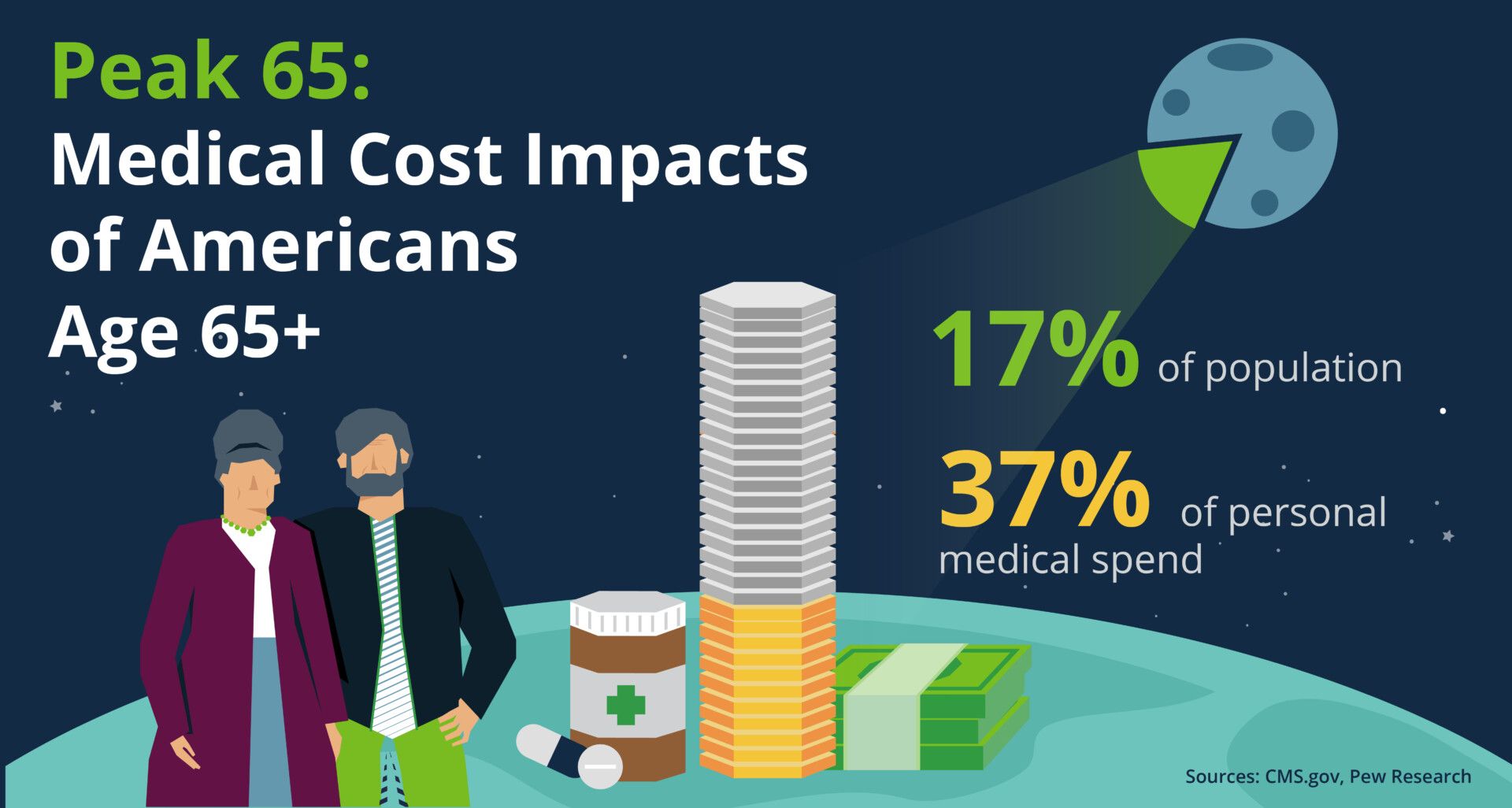

It’s no secret that the alphabet soup of Medicare options can feel complicated and confusing – the CCD says that 33% of Medicare-eligible employees do not realize that Medicare is a viable option. With people over age 65 accounting for up to 37% of personal healthcare spend in the US, it’s beneficial for both the employees and employers to find the right fit of medical benefits for this growing employee group.

In this blog we’ll touch on how this impacts employers, the basics in Medicare options and timelines, and next steps to set your employees, and your company, up for success.

| At-a-Glance Read time: 5 minutes |

||

|---|---|---|

How Does This Impact Employers?

Medicare will affect everyone at some point in their lives. This vital resource can provide critical coverage for everything from annual exams and prescriptions to hospital stays. Having the proper coverage can have significant financial impact, which is especially true when people age 65+ often see some of the highest claimant costs. The average employer saves $18,000 per employee who transitions to Medicare (Brown & Brown). Both the physical and financial wellness of employees can be impacted by these decisions, as well as the employer's medical expenses, especially in industries with higher rates of aging employees.

| Due to an aging workforce, a manufacturing company was looking into all cost-savings options. A Medicare specialist was brought in to conduct side-by-side comparisons of the employer health plan and Medicare options when employees turned 65 and were still working. This allowed employees to enroll in the most cost-effective coverage that fit their individual needs. As a result, it also offered cost avoidance for the employer. Employees enhanced their benefits and reduced out-of-pocket costs. The solution provided mutual benefit for both employer and employees. |

Population health management platforms are also a resource that can use data analytics to review the effectiveness of medical plans and help assess how they compare to Medicare options. In combination with education from a Medicare specialist and resources for employees, this can lead to beneficial results for both the employee and plan provider.

Understanding the Medicare Alphabet Soup

Human resources teams are critical in guiding employees through their benefit options, but when it comes to Medicare, HR is not equipped to counsel employees directly. That is where a Medicare specialist comes in. However, here are the basics of Medicare:

Medicare Part A covers inpatient / hospitalization and expenses related to a hospital stay.

Medicare Part B covers a whole list of outpatient / medical services.

Medicare Part C, also known as Medicare Advantage, provides additional coverage such as vision, hearing, dental, and wellness programs, with many also including prescription drug coverage.

Medicare Part D provides outpatient prescription drug coverage as a stand-alone if an individual is not already receiving this coverage through a Medicare Part C plan.

Medicare Medigap includes a whole range of letters that are supplemental insurance policies to help pay out-of-pocket cost for Parts A and B.

Why Choosing the Right Coverage Matters

When someone files for Social Security benefits, they are automatically enrolled in Medicare Parts A and B. However, they can choose to opt out of Part B if an employer plan covers them or they have insufficient credits. There are some risks to dropping coverage that employees should investigate and consider, including potential gaps in coverage and late enrollment penalties. This Medicare.gov fact sheet has more details on how employees can get started navigating these important decisions.

If the employee has not yet filed for Social Security, they can enroll in the enrollment period that runs from three months before until three months after their 65th birthday. Or they can wait to enroll until they stop working. Medicare.gov offers more insights on signing up for Medicare for employees who are working past 65.

Next Steps for Employers

Employers can play an important role in setting their employees up for success.

- Ask your benefits consultant to review your data. A population health analytics platform can give valuable insights to your demographics to determine if working with a Medicare specialist is right for your organization, which could provide opportunities to reduce overall costs to your healthcare plan.

- Work with a Medicare specialist. A specialist helps bridge educational information about your medical plan and what is available through Medicare, giving employees a clearer understanding of their options and associated costs to pick the plan that is best for them. Providing educational resources to employees helps them decide what plan is right for their needs and when applicable navigate a successful transition from their employer plan to the right Medicare plan, all while potentially saving the company money.

- Create a communication plan. Use the Medicare enrollment timeline as a guide to help you create a plan for communicating to your employees about educational opportunities and important reminders. Your Medicare specialist can also help you establish a messaging plan.

The good news is that there are resources to navigate these important decisions. Woodruff Sawyer partners with professional organizations to help clients evaluate their employee's coverage needs and navigate their Medicare options. This teamwork can result in the same or better coverage with Medicare at significant savings to both the employee and employer.

Authors

Table of Contents