Blog

SPAC Litigation Outlook: 2021 Trends Lead to 2022 Predictions

Yelena Dunaevsky

Yelena Dunaevsky

Jan 20, 2022

Jan 20, 2022

Read more for our predictions for SPACs in 2022, based on what we saw and analyzed in 2021.

There was no shortage of excitement and drama in the world of SPACs in 2021. The year started with IPOs of hundreds of SPACs in numbers that eclipsed everyone’s expectations. The exuberance in the SPAC market in the first quarter attracted so much attention from investors, media, and regulators that by April, investors were tapped out, the media’s storyline turned sour, and SEC’s statements around the treatment of warrants brought the market to a halt. IPO activity dropped by 90%, and what many at that time considered a minor hiccup lasted well into the Fall. In September and October, we finally saw increased signs of activity both on the IPO and business combination (de-SPAC) sides of the market. The year finished out with multiple deals pricing, many closing, and a good number of SPACs announcing combinations that should close in early 2022.

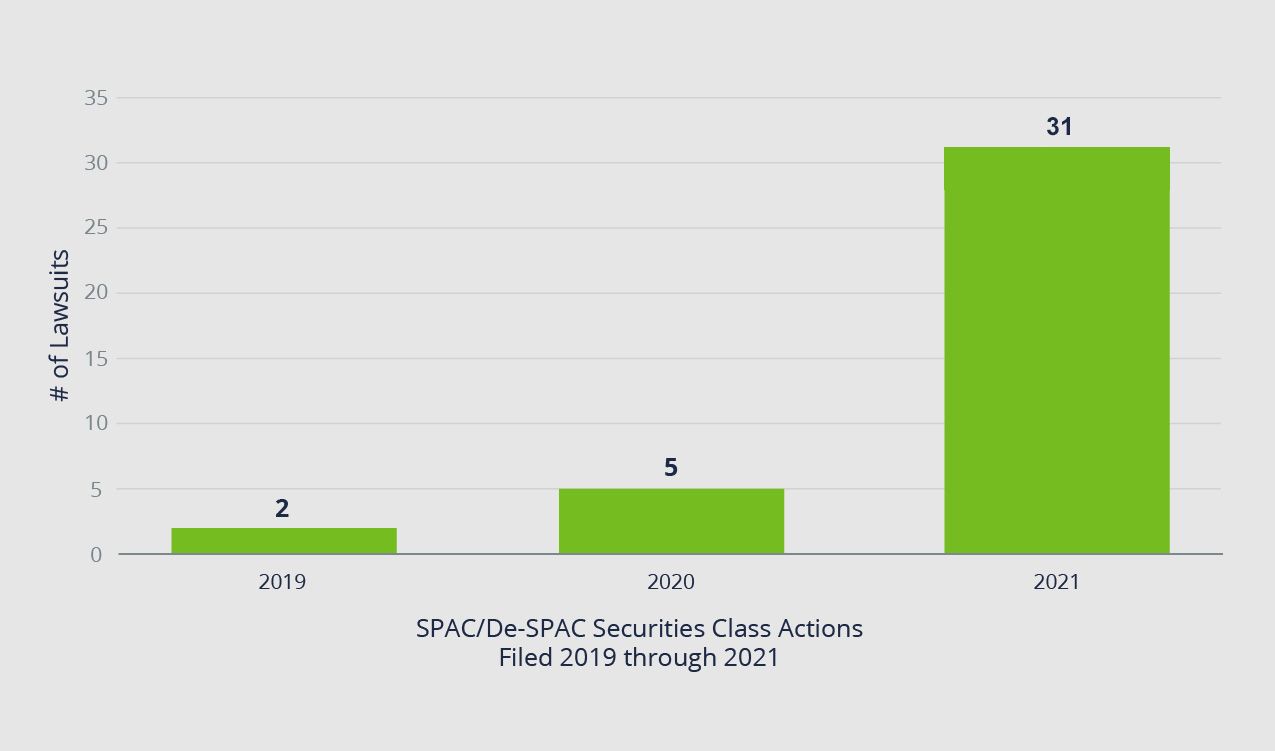

Plaintiff’s bar was also paying close attention. The types and the number of lawsuits increased dramatically in 2021 as compared to 2020 and previous years. According to the data collected by Woodruff Sawyer, securities class actions filed in connection with SPAC-related transactions in 2021, for example, jumped by 520% from 2020.

SPAC Securities Class Actions

Source: Woodruff Sawyer

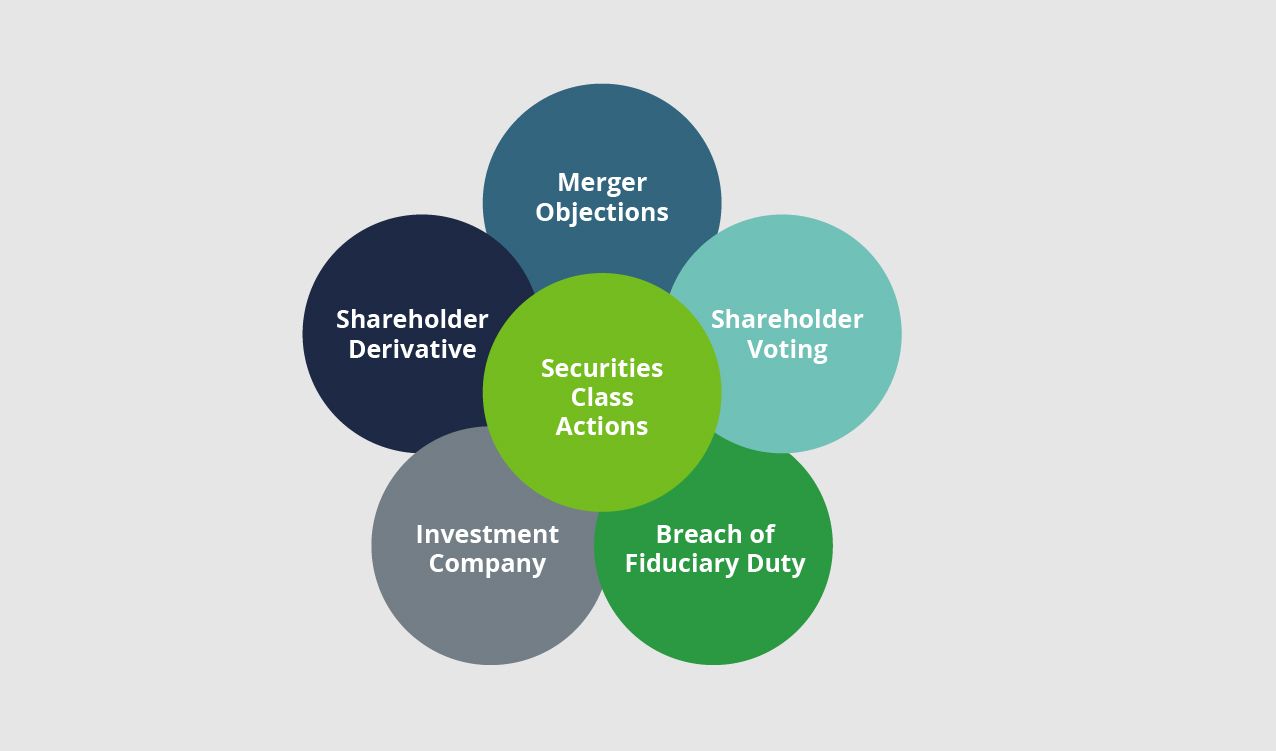

Furthermore, we observed at least six different types of lawsuits brought against various SPAC-related entities and individuals in 2021. They included merger objection lawsuits, securities class actions, breach of fiduciary duty suits, shareholder derivative suits, investment company suits, and shareholder voting suits.

Six Types of SPAC Lawsuits

Source: Woodruff Sawyer

The most common type was the merger objection lawsuit, which affected approximately 30% of SPACs that announced and completed their business combinations. In the SPAC context—much like in non-SPAC deals—as soon as a deal is announced, a plaintiff files a suit claiming that the deal is unsatisfactory in some way and should not proceed. The allegations usually revolve around insufficient disclosure about the upcoming merger.

In response, SPAC parties typically file additional disclosure with the SEC, the suit becomes moot, and the plaintiff and their attorneys walk away with a “mootness fee” of a few thousand dollars. Despite their frequency, merger objection lawsuits are not creating as much anxiety for SPACs as the ever-growing number of securities class actions (SCAs).

Litigation Outlook for 2022

SCAs are usually the most severe of the six types of lawsuits mentioned above in terms of defense time and costs. These suits can be brought in federal or state court against the SPAC, its directors and officers, or the private company being acquired by the SPAC, and its directors and officers. In some cases, SCAs name SPAC sponsors and other related deal parties as defendants.

Depending on the fact pattern, allegations in these kinds of suits center around violations of the Securities Act of 1933 or the Securities Exchange Act of 1934 and typically focus on misstatements or omissions in the disclosure or other public statements.

Of the 31 SCAs filed against SPACs in 2021, 20 were brought within six months after the close of the SPAC’s business combination and the average time it took to bring a lawsuit was nine months.

Interestingly, two of the 31 SCAs brought in 2021, the Lucid Motors case and the Stable Road/Momentus case, were commenced prior to the completion of the merger. The December 2021 lawsuit brought against the CEO of Digital World Acquisition Corporation, which has plans to merge with Trump Media and Technology Group, was not an SCA but was also brought prior to the proposed merger.

Securities Class Action Predictions for 2022

Of 197 business combinations that closed in 2021, 16 have been subject to an SCA. Out of these 16, ten were filed in the fourth quarter of the year and the time between the merger and the filing of the lawsuit for these ten SCAs averaged 4.6 months. If SPAC-related SCAs continue to be filed at the same pace as in Q4 of 2021, we anticipate seeing at least 40 SPAC-focused SCAs in 2022.

Based on trends from 2021, we also anticipate seeing SCAs filed against a disproportionate number of SPACs in the electric vehicle space. Out of the 197 completed business combinations in 2021, 17, or almost 9%, were done by companies in the electric vehicle industry. However, out of the 31 SPAC-related SCAs in 2021, 10, or over 32%, involved electric vehicle companies.

Another trend from 2021 that we will continue to watch and will likely gain additional traction in 2022 are SCAs that are filed shortly after a publication of a negative short seller report (discussed below).

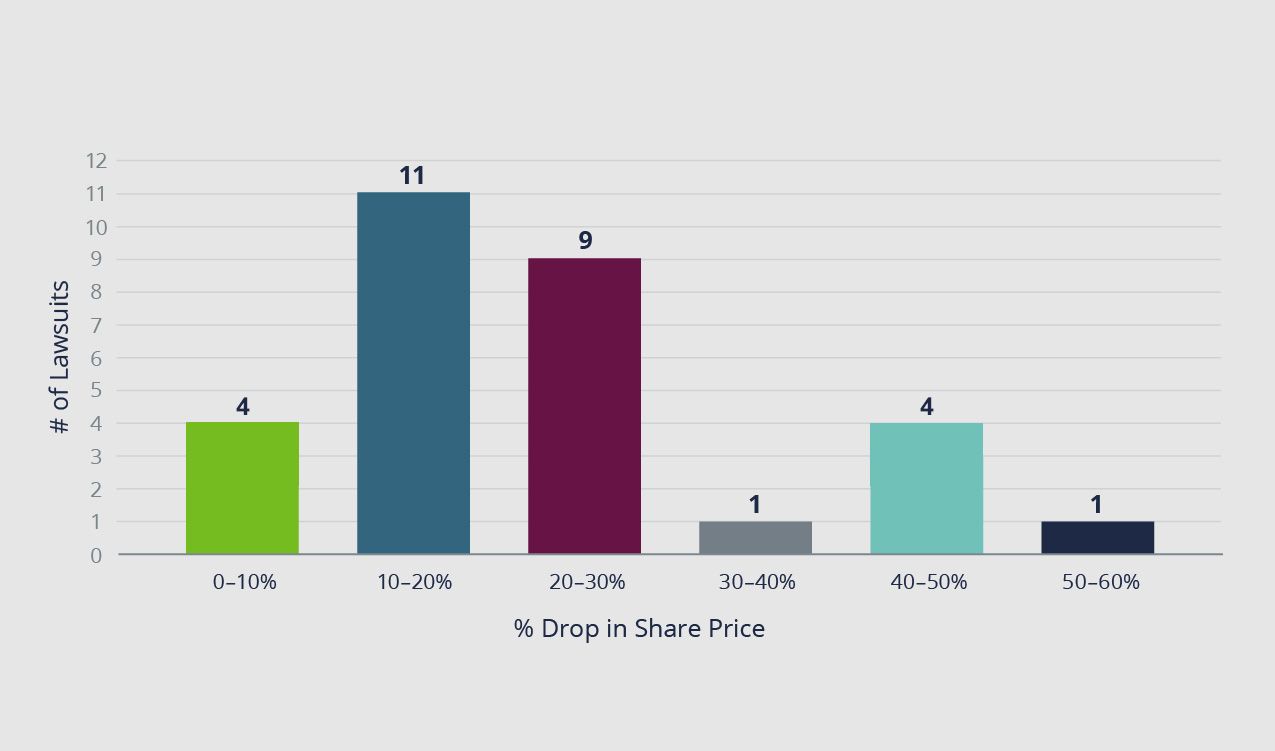

Price Drops and Short Seller Reports

One of the most common causes for these lawsuits is the drop in the share price of the SPAC’s shares before the merger or the combined company’s shares after the merger. The stock price drops we observed in the SCA suits in 2021 ranged from 4% to 56%, with the average being around 22%.

SPAC Stock Price Drops in 2021

Source: Woodruff Sawyer

Many price drop incidents follow a short seller’s report, and some come on the heels of a disappointing earnings announcement. Out of the 31 lawsuits in 2021, ten, including the one from November of 2021 against Ginkgo Bioworks Holdings, were filed after a short seller report publication claiming problems at the company. Interestingly, the price drops in lawsuits brought after a publication of a short seller report were lower on average with the majority being in the 10%-20% range.

Short seller reports in 2021 were issued by several firms, including the Hidenburg Research and Muddy Waters. The SPAC-related lawsuits that followed these reports alleged issues with financials disclosures and representations related to customers or sales. For example, Hidenburg Research issued a report in March of 2021 covering Lordstown Motors and alleging that the company’s statements about the pre-orders for its electric vehicle truck and its production projections were false.

Enforcement and Legislative Outlook for 2022

Lawsuits were not the only actions launched against SPAC-related transactions in 2021. The Securities and Exchange Commission (SEC) and, in particular, SEC Chair Gary Gensler have been very vocal throughout the year, issuing statements and speaking out against insufficient disclosure and questionable marketing and diligence efforts adopted by some SPACs. In a December 9, 2021 speech, for example, Chair Gensler, spoke about strengthening disclosure requirements for SPACs and protections for SPAC investors. In an April 2021 statement, John Coates of SEC’s Division of Corporation Finance surprisingly questioned SPACs’ reliance on the Private Securities Litigation Reform Act (PSLRA) safe harbor for forward-looking statements.

The SEC backed its concerns with several enforcement actions. In July 2021, for example, it charged a SPAC, the merger target, both entities’ CEOs, and the SPAC’s sponsor with misleading disclosures ahead of their merger. Some of the parties settled, and total penalties amounted to more than $8 million. Similarly, in October of 2021, the SEC also settled a fraud action it filed against a SPAC in 2020, and in December 2021 another action it filed against a SPAC in 2021. The first settlement amounted to $38.8 million and the second to $125 million.

In 2021, based on publicly available information, the SEC filed or settled at least four SPAC-related actions while the DOJ and FINRA between them conducted at least three investigations into SPACs. A highly publicized FINRA investigation at the end of 2021 revolved around its inquiries into Digital World Acquisition Corporation (DWAC) and its merger target, Trump Media and Technology Group (TMTG). According to DWAC’s December 6, 2021 Form 8-K, it received a request for information from FINRA relating to events prior to its announcement of its merger. The SEC also requested documents relating to meetings of DWAC’s Board of Directors, policies and procedures relating to trading and other matters and communications between DWAC and TMTG.

Legislators have also taken notice of the increase in SPAC activity in 2021. Senator Elizabeth Warren, for example, called on the SEC in November 2021 to investigate the DWAC TMTG deal for possible securities violations. Warren and several other senators also sent letters in September 2021 to six SPAC creators outlining their concerns about potential misaligned incentives between SPACs’ creators and investors.

On November 9, 2021, two pieces of legislation aimed at imposing additional regulations on SPACs were introduced in the US House of Representatives. The first is H.R. 5910, the “Holding SPACs Accountable Act of 2021,” sponsored by Rep. Michael San Nicolas (D-GU) and the second is H.R. 5913, the “Protecting Investors from Excessive SPACs Fees Act of 2021,” sponsored by Rep. Brad Sherman (D-CA).

All this activity and the continuing focus on SPACs will undoubtedly lead to additional investigative and enforcement actions from the SEC, DOJ, and FINRA. Additional regulations aimed at SPACs are very likely in 2022 but although rule amendments related to SPACs are on the SEC’s agenda slated for April of 2022, nothing specific has yet been proposed.

Enforcement and Investigation Predictions for 2022

We predict at least 25 various enforcement and investigative actions in 2022 if all SPACs that are waiting to announce a business combination actually do so. Multimillion-dollar penalties and settlements are extremely likely.

The severity and frequency of securities class actions and regulatory enforcement actions aimed at SPACs and their related parties have a direct impact on the availability and pricing of directors and officers (D&O) insurance. This insurance is instrumental in attracting and retaining qualified independent directors for both the SPAC and its post-merger public company. Availability and pricing of public company D&O insurance for SPAC-related entities became extremely strained in 2021 because of the number of SPACs completing their IPOs and de-SPACing in 2021. It was further constrained by record numbers of traditional IPOs in 2021.

If additional D&O insurers enter the SPAC market or existing carriers expand their underwriting appetite and capacity in early 2022, availability and pricing of this insurance product may improve later in the year. We, at Woodruff Sawyer, are watching SPAC-related litigation and enforcement developments as well as the ongoing changes in the SPAC insurance market very closely and will be addressing them and the best ways to approach the D&O insurance market in our future SPAC Notebook articles.

Visit our SPACs industries page for more insights and resources related to Special Purpose Acquisition Companies.

Author

Table of Contents