Blog

Implementing “Highly Protected Risk” Programs Will Lower Property Insurance Costs

Sep 07, 2022

Sep 07, 2022

"Highly protected risk" (HPR) is an insurance industry term referring to a risk that has been controlled and managed through various measures.

The International Risk Management Institute describes a highly protected risk property as one that is much lower than normal probability of loss. This could be by virtue of being a low-hazard occupancy or property type and having superior construction, special fire protection equipment and procedures, and management commitment to loss prevention.

FM Global, a property insurance company, describes an HPR location as one in which all reasonable physical and human element loss-prevention measures have been implemented to protect buildings, equipment, and contents from all losses, including those caused by natural hazards.

Insurance carrier underwriters work to ensure their clients' HPR account risk profile remains stable, year to year. The carriers look for the policyholder’s risk management team to adhere to HPR guidelines and allow the carrier’s engineering consultants to actively monitor and contribute toward the client’s loss-reduction efforts.

Although it can be a costly and time-consuming process, properties that achieve HPR status tend to have fewer losses and hence, can expect lower premiums on their commercial property insurance. This reduction is cumulative over the life of the property.

The Human Element: A Key Contributor to HPR Classification

Human element risk-reduction efforts involve a performance-based approach to maintaining and updating a structure, its operations, and the fire protection systems. Human element programs are designed to control ignition sources, minimize flame spread, manage the presence of combustibles, and ensure that fire protection systems function as designed.

The National Fire Protection Association (NFPA) reports that human element factors play a significant role in most fires and explosions. Statistical studies of loss incidents in a variety of industries have indicated the following general breakdown:

Factors affecting loss incidents:

- Human factors (70-80%) (e.g., management program deficiencies, human operator errors)

- Equipment failures (10-20%) (e.g., design or maintenance deficiencies)

- External factors (10-20%) (e.g., earthquakes, floods)

A small sample of the human element programs that apply to a wide variety of industry segments includes:

- Fire protection systems inspection, testing, and maintenance

- Fire protection systems impairment

- Electrical systems testing and maintenance

- Hot work permit systems

- Equipment predictive maintenance

- Housekeeping and storage

- Industrial control systems

- Physical security controls

- Business continuity planning

The National Commission on Fire Prevention and Control's "America Burning" report finds that well over half of the major fires within all industry segments are due to some form of human oversight. These human-driven losses have resulted in an average of 3,900 civilian deaths annually over the past three years and up to $10 billion in direct property damage on an annual basis.

Engineering Controls: First Line of Defense in Protecting Properties

Property insurance carriers employ a non-traditional business model whereby risk and premiums are determined by engineering analysis—as opposed to historically based actuarial calculations. These carriers operate from the philosophy that most losses can be prevented. They provide insurance products and property loss prevention engineering services to protect their clients.

Fire protection engineering guidelines developed from scientific studies take both a prescriptive and performance-based approach toward the implementation of controls to better protect properties, minimize machinery failures, and better safeguard processes. These fire protection engineering controls are implemented to prevent the development of ignition sources, identify the correct fire-protective systems based on the level of exposure, minimize flame spread, and isolate smoke and fire to minimize potential damage.

Fire protection engineering research focuses on the analysis and control of special hazards, which in many cases represent the proximate cause of all large property losses in the United States. Fire protection uses physics-based models of fire scenarios and their effects on structural and non-structural building elements to predict risks and identify loss-mitigation efforts.

Fire protection engineering controls include, but are not limited to, the following:

- Substantial construction

- Well-protected special hazards

- Adequate sprinklers, water supply, detection/alarm systems, special protection systems

- Adequate human element programs in place and maintained

- Minimal exposure from natural hazards or adequate mitigation

- Minimal risk from external exposures based on construction and/or separation

Engineering controls should be the first line of defense in protecting properties and minimizing potential loss.

What's the ROI on Costly HPR Controls?

Achieving the HPR level of protection often requires analysis or a return-on-investment study since engineering-type controls, which go beyond municipal code requirements, can be very costly to implement. Management must consider the physical property loss cost-benefit and the business continuity cost benefit.

Compliance with human element programs and guidelines typically does not require a significant expenditure to complete. These loss-prevention measures are often considered low-hanging fruit, since the implementation and ongoing management of such programs require only a time commitment from the in-house facilities/engineering staff and in some cases, a minor expense due to third-party resource involvement.

Property carriers and property brokers typically have in-house property engineers who audit a client’s approach toward HPR status and assist the client in complying with carrier recommendations. Third-party resources are also used to assess HPR compliance.

The carrier and/or third-party resources conduct site surveys to determine whether a client’s risk exposures and property management controls are in line with HPR property and regulatory agency guidelines. If they encounter deficiencies, carriers will provide risk-reduction recommendations in hopes of bringing the risk to an acceptable HPR level. Underwriters will often accept alternative and less-costly solutions to the recommended engineering controls if human element controls are in place.

What about your return on investment (ROI)? Loss prevention will grant the property holder access to lower rates for property risk insurance. As a risk’s “protection” increases, underwriters can commit to greater capacity, often at a better price with broader contract terms.

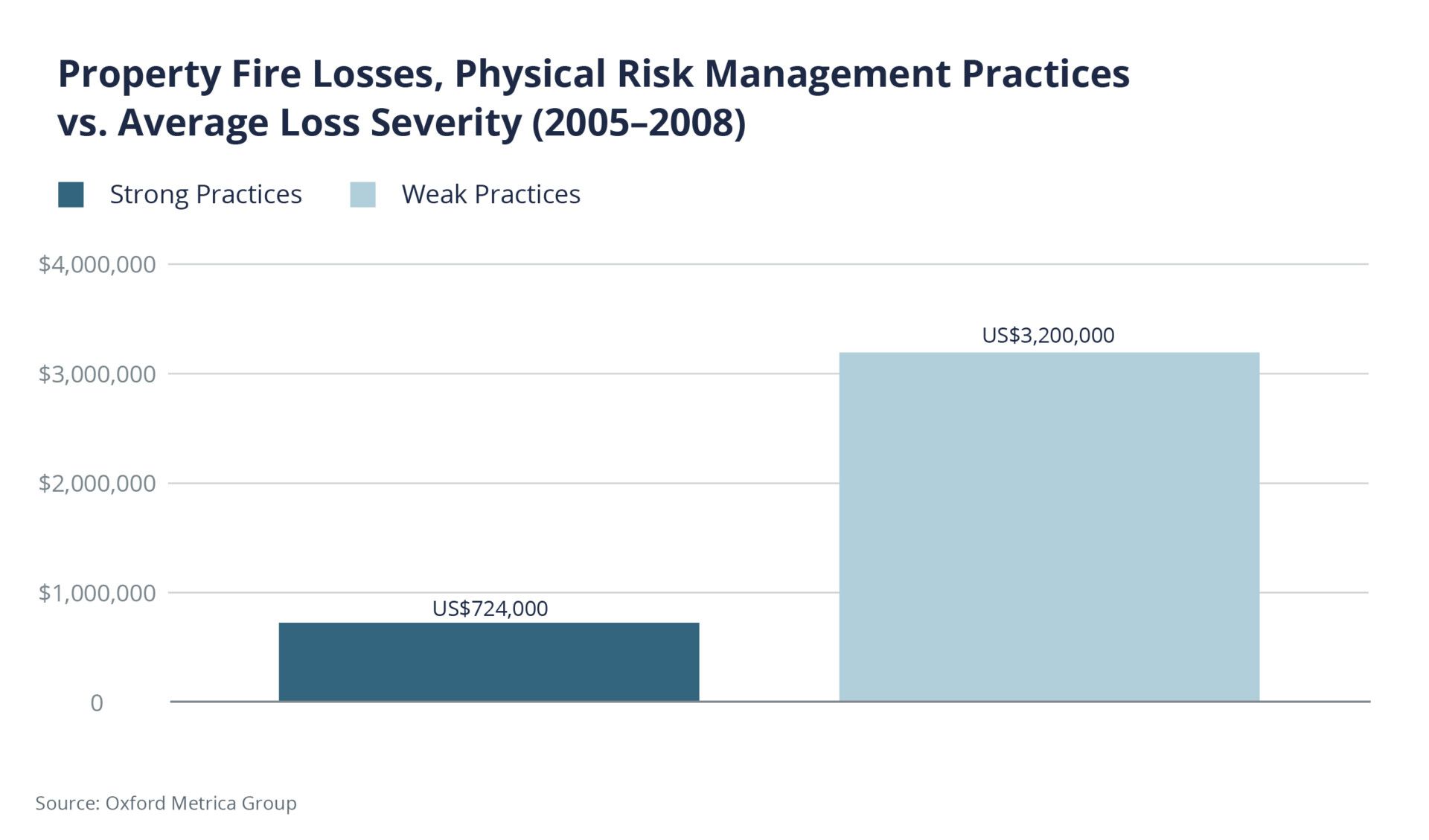

The benefits of achieving HPR status go beyond lower insurance costs. The Oxford Metrica Group released a study finding that companies that implement physical risk management practices (enterprise risk management & HPR loss-prevention programs) experience fewer losses, incur lower total incurred loss dollars, and offer a stable, more consistent value to shareholders. Reducing your exposure to loss does more than build resilience. It empowers a company to command the best insurance coverage at the best terms. The HPR level of property protection can provide peace of mind in that your facility meets the highest industry standards for property protection.

Reducing your exposure to loss does more than build resilience. It empowers a company to command the best insurance coverage at the best terms. The HPR level of property protection can provide peace of mind in that your facility meets the highest industry standards for property protection.

Have the Right Resources Ready

If you're thinking about loss prevention or are interested in taking steps to control your property risk, knowing where there are resources to help you is essential.

FM Global develops Property Loss Prevention Data Sheets that are based on scientific studies conducted at its laboratories, through analysis of third-party property loss prevention study findings, and through the adoption of various nationally recognized NFPA codes. These Data Sheets identify engineering and human element loss-mitigation measures for commercial and industrial property environments, which when achieved, qualify a risk as meeting HPR status.

Contact the Woodruff Sawyer Property Engineers if you have any questions regarding HPR property conservation or are interested in how we can lower your risk of loss.

Author

Table of Contents