Blog

How Well Do You Understand Your Lease and Insurance Obligations During a Claim?

Emanuel Enes

Emanuel Enes

Mar 01, 2018

Mar 01, 2018

Once in a while, I come across unique requests from clients (especially those who are real estate developers or owners), where the landlord or the tenant wants to shift insurance obligations in the lease from one to the other. This action can be tricky, because critical lease clauses –if not carefully reviewed by a broker--can cause real problems in the event of a claim.

The Importance of Reviewing Leases for Potential Liability

As a claim consultant focused on property liabilities, I review clients’ leases as part of my standard process in assessing their risk exposures. It’s important for companies to have their brokerage firm conduct a careful review of the critical lease clauses that impact a property owner’s obligations in the event of a claim, for several reasons:

- To assess the client’s property exposure with regards to tenant improvement and betterments (TIBs).

- To assess the client’s contractual obligations and compliance with lease requirements.

- To understand the client’s desired level of involvement/expectations should a loss occur.

Shifting Insurance Obligations Often Results in Over-Insuring Property

In many cases, when a landlord or tenant wants to shift insurance obligations, they end up with mutual obligations to insure; some over-insure, and others may unintentionally create gaps by under-insuring. Over-insuring can occur when both the landlord and tenant purchase insurance for the same property, i.e., the landlord purchases insurance for tenant improvements/betterments (TIBs), normally insured by the tenant, and common area that would normally be insured only under the landlord’s master policy.

Under-insurance can occur when either party assumes the other will insure property based on their interpretation of the lease, which may not be consistent with the other party’s interpretation and intent. As such, situations could arise where both buy coverage or neither buys the coverage needed.

In one case, we had a property owner who wanted to have “complete” control of the repairs in a claim situation. But, rather than simply enforcing the terms of their lease and requiring the tenant perform the repairs to the TIBs, they actually wanted control over insuring and repairing the landlord-owned property and tenant improvements regardless of when it was installed or who paid for them.

However, their current lease language was the common type, where a landlord insures the common property and pre-existing improvements, and tenants should insure their newly installed TIBs until they vacate, insure their personal property and business interruption.

When the language of the lease does not give the landlord full control of the repairs, including TIBs, the landlord may encounter a situation where later they are not able to recover from the tenant for costs incurred on repairs to TIBs, and they may create an exposure for liability if damage or theft occurs to the tenant’s property during the course of the repairs they are overseeing.

Although it’s important to act promptly to mitigate the damages after an incident, it’s equally important to abide by the terms of the lease contracts to avoid creating additional liability exposure or claims coverage issues.

Avoid Claims Issues through Proper Lease Terms

Given that over-insuring or under-insuring tends to be a problem in certain situations as outlined in the previous section, let’s look at some things to watch for in a lease to avoid this issue.

It’s important not to confuse the “tenant repair” obligations language with the “insurance” obligations in the event of a casualty such as fire, domestic water line break, storm, etc.

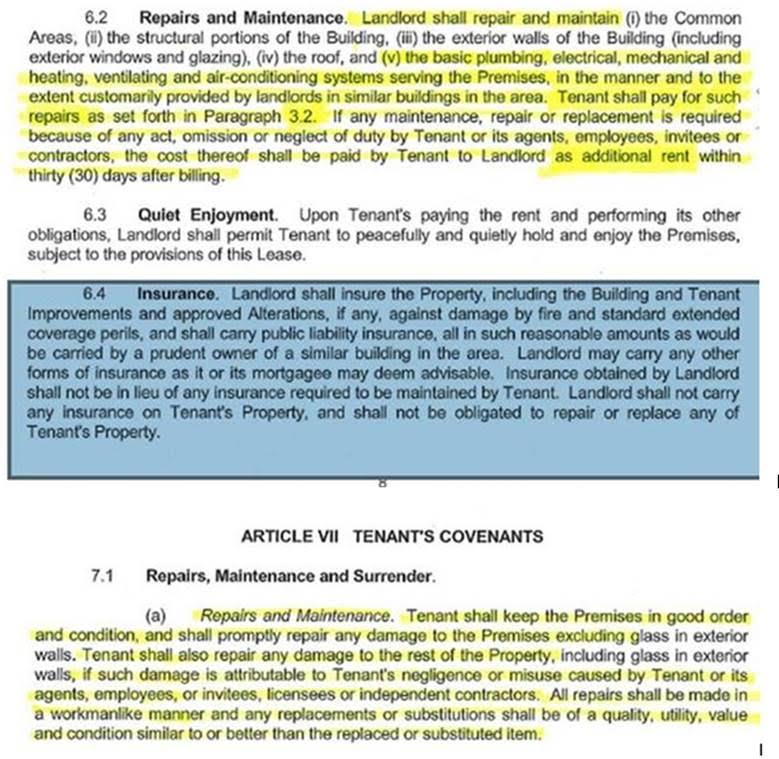

One of the most commonly misinterpreted clauses in a lease is the “Repairs and Maintenance” obligations. This clause spells out expectations for the day-to-day maintenance of the premises, such as cleaning the sidewalk, cleaning the windows and it may include maintenance of HVAC unit, etc.

The repair language is meant to deal with everyday maintenance issues. However, it’s the “Insurance” clause that controls in a claim situation, along with any “waiver of subrogation” language in the lease. The “Tenant Improvements” clause in the lease exists in part to address installation of improvements, the ownership and time when title will transfer, and who pays the taxes on TIBs, etc.

A Cautionary Tale

When there is a fire or water line break, it’s not a “Repairs and Maintenance” issue, it’s a “casualty” issue governed by the “insurance” language of the lease. Although both instances require repairs, the party required to perform and pay for those repairs is not the same: common daily maintenance repairs are the obligation of the tenant while casualty repairs to common property are commonly the landlord’s obligation.

One client of ours undertook all the repairs for water extraction to their leased space based on their internal interpretation of the lease before reporting the loss to us and having us do a full lease review.

The client undertook all the cost of the repairs to both landlord and tenant improvements, expecting the insurers would later sort it out. However, once the repairs were all completed and paid by the landlord, the act of seeking recovery from the tenant or its insurer is deemed subrogation.

Since the lease contained a mutual waiver of subrogation, the insurer for the tenant denied the landlord’s claim seeking equitable reimbursement for cost incurred on TIB repairs on behalf of the tenant. The waiver of subrogation clause precludes the pursuit of a recovery between the landlord, tenant, or their insurers after the vendor(s) is paid.

This could have been avoided by understanding how a Waiver of Subrogation clause can trump some of the other clauses in the lease, and by only assuming responsibility and incurring costs for repairs where you have an insurable interest.

Both landlord and tenant can use the same vendor for the repairs, but each should request their own estimate and invoice for their respective interests, and claim submission to their insurer.

A sample of that lease language follows. Note how they highlighted everything (at 6.2) in the “Repairs and Maintenance” before the “insurance” provision; they selected the wrong language because the repairs and maintenance reference deals with the day-to-day upkeep, not a casualty/claim. The parties overlooked the obvious “insurance” provision, which basically indicated that as a tenant they did not need to take action since the landlord had assumed ALL responsibility (at 6.4) except for the tenant’s office furniture.

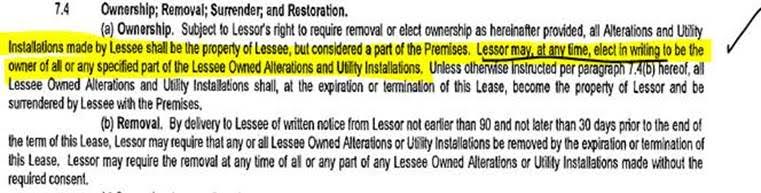

When Landlord is Owner of TIBs “At Any Time”

While reviewing a different lease for another client, this next clause below is not common, but is quite interesting, because the lease allows for the landlord to communicate “the landlord is the owner of the TIBs” at any time.

Not all Repairs and Maintenance clauses read the same; nonetheless, their intent is to address who is responsible for daily maintenance of the premises, not to shift responsibility for repairs after a casualty incident such as a fire, common area water line break, storm damage, etc.

Depending on the size of the loss or degree of control the landlord desires to exercise, the landlord can simply notify the tenant in writing “at any time” to be the owner of the lessee owned alterations and utility installations. Therefore, the landlord can make the election before a loss, during the loss repairs or any time it is not satisfied with how the restoration is undertaken by the tenant.

As such, the landlord can do this after a loss and take control of the repairs to their property and TIBs without having to wait on the tenant’s insurer to allocate between the two policies. The insurers are bound by the lease’s agreement terms their insureds sign before a loss.

For the landlord’s insurer, this could significantly increase their exposure during the restoration period of a loss, if the landlord exercises this right mid-claim—the landlord’s insurer could end up funding all the repairs to the common area owned by the landlord, and TIBs that were owned and insured by the tenant.

Landlords, tenants, and property managers should have a clear understanding of the lease terms and how the clauses impact one another. If one party makes changes in a clause at some point, then a review of the other dependent clauses should also be undertaken.

A well written lease helps the parties procure the correct insurance to avoid coverage gaps, under-insurance, over-insurance, or inequitable exposure transfer to an insurer when a party exercises their lease contract rights.

Next Steps in a Claim

Once a claim is on notice to the broker and insurer, it’s important for the claim professionals and client to work collaboratively and agree on the lease interpretation. Then, everyone must make sure their intentions align with the client’s understanding and expectations, and these must be communicated to the vendors performing the clean-up restoration and repairs for the scope of work/estimate to be accurate for each party, and for invoices to allocate the costs to the correct party bearing the risk.

The insurer is the final decision maker on coverage. Therefore, it’s beneficial for everyone to understand who is responsible for the repairs, has authority to approve vendor’s work, and will ultimately be invoiced for the work and payment to the vendors.

As a property owner, it’s prudent to take action and mitigate the loss, but it’s not your responsibility to mitigate the tenant’s loss.

If there is mutual waiver of subrogation, are you prepared to incur the costs on behalf of the tenant and not be reimbursed by your insurer (no insurable interest) nor be reimbursed from the tenant’s insurer (precluded from seeking recovery due to subrogation waiver)?

Early lease review, identification of the issues, involvement by the claims professionals and interested parties is critical to setting clear expectations and a successful recovery on the claim for costs incurred.

A careful review of the lease’s critical provisions and understanding your level of involvement in the claim process and supervision of repairs will make a significant difference in properly understanding your insurance needs, contractual obligations and meeting the other parties’ expectations.

Author

Table of Contents