Blog

The Problem with Storage Tanks: What you Need to Know to Own or Operate

Aug 08, 2019

Aug 08, 2019

The goal of this article is to provide you with the information you absolutely need to know if you (or your organization) own a storage tank.

The goal of this article is to provide you with the information you absolutely need to know if you (or your organization) own an underground storage tank, or UST. Many people are not aware, but the term underground storage tank (UST) is a bit misleading. The EPA defines a UST as "a tank and any underground piping connected to the tank that has at least 10% of its combined volume underground." What does this mean? A storage tank visibly above ground could actually be classified as a UST and be subject to regulations and requirements that ASTs (aboveground storage tanks) are not subject to. The adage that there is "more than meets the eye" is quite true when it comes to USTs. So, what's the problem with storage tanks? Well, there are quite a few:

- They leak, which poses a significant threat to public health and natural resources.

- Leaking tanks can lead to very expensive cleanups, bodily injury and property damage claims, and business interruption expenses (third and first party).

- Estimates suggest there are tens of thousands of USTs currently leaking around the United States.

- USTs become very difficult to insure after 20 years of use, making financial responsibility compliance difficult for tank owners.

- Government regulation and the insurance marketplace are out of sync and lacking in information and education for tank owners/operators, which leaves them unprepared and exposed.

- There are a lot of USTs, which are currently necessary.

In Washington State alone, the state Pollution Liability Insurance Agency, or PLIA, estimates there are roughly 2,900 leaking USTs. From 1988 to September 2016 there have been 532,420 confirmed leaks/releases from USTs in the United States, and 461,441 cleanups have been completed. I think the most significant problem is the lack of rapport between the government (regulation), the insurance marketplace (financial responsibility), and tank owners. The result is a lack of information that leads us toward some problems for tank owners.

A Brief History of Underground Storage Tanks

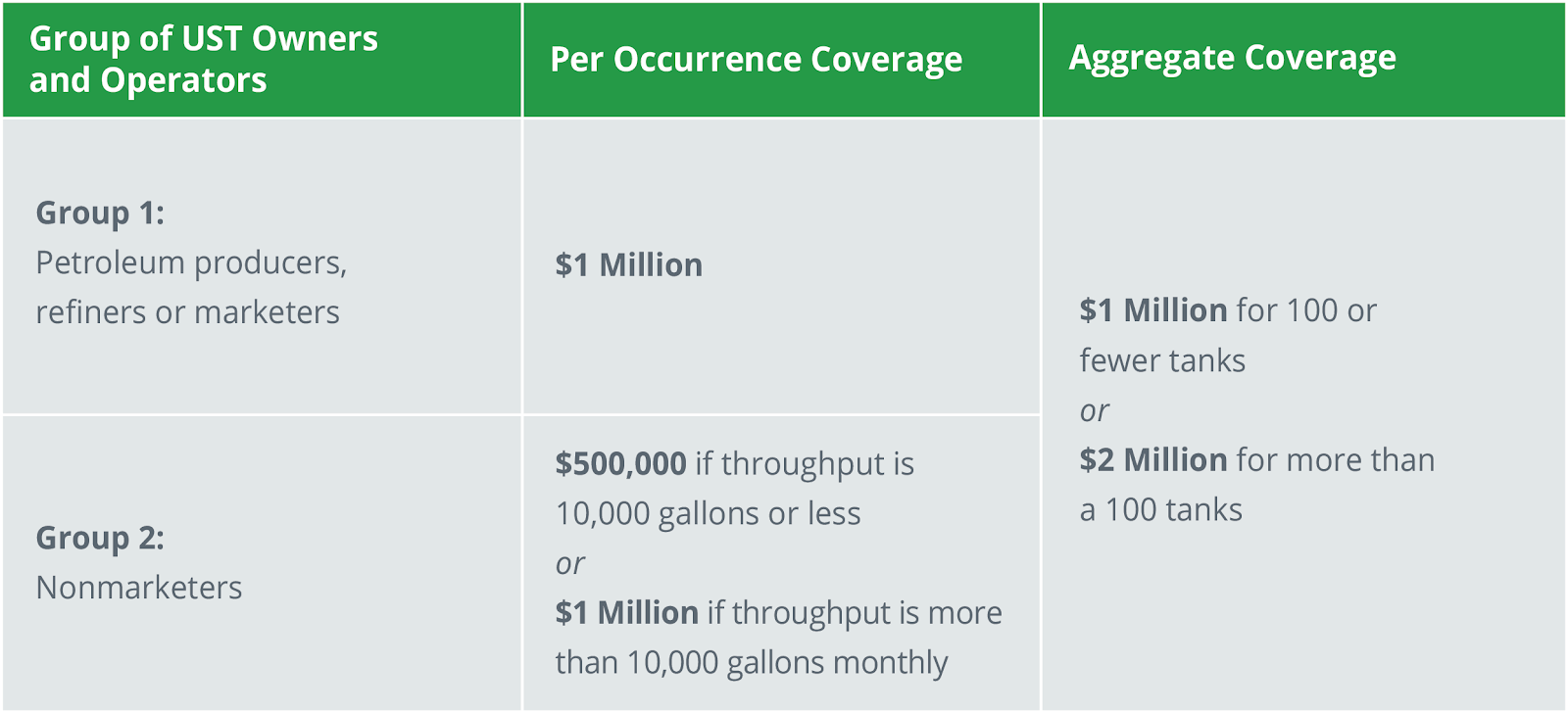

In 1984, Congress created a federal program to regulate USTs containing petroleum products and hazardous chemicals in an effort to minimize future tank leaks. Prior to this, most USTs were made of bare steel, which corrodes over time, resulting in leaking tanks. The legislation allowed the EPA to set standards for tank design, installation, leak detection, spill and overfill control, corrective action, and tank closure. Two years later, in 1986, the EPA established financial responsibility requirements for UST owners and operators intended to cover the cost of taking corrective action and to compensate third parties for any damages caused by leaking tanks.  There are several ways for a tank owner/operator to evidence financial responsibility (please note that some states have additional restrictions. Check your state regulations to make sure you are compliant). The most common and cost effective method is a storage tank insurance policy. Other methods include a corporate guarantee, surety bond, letter of credit, setting aside the required amount in a third-party administered trust fund, or demonstrating self-insurance using a financial test. For many organizations the only feasible solution is insurance, which is the focus of this article. If your organization is able to self-insure, provide a corporate guarantee, or letter of credit, long term, those may be your best options to minimize any potential impacts to your operations resulting from non-renewed insurance coverage due to tank age.

There are several ways for a tank owner/operator to evidence financial responsibility (please note that some states have additional restrictions. Check your state regulations to make sure you are compliant). The most common and cost effective method is a storage tank insurance policy. Other methods include a corporate guarantee, surety bond, letter of credit, setting aside the required amount in a third-party administered trust fund, or demonstrating self-insurance using a financial test. For many organizations the only feasible solution is insurance, which is the focus of this article. If your organization is able to self-insure, provide a corporate guarantee, or letter of credit, long term, those may be your best options to minimize any potential impacts to your operations resulting from non-renewed insurance coverage due to tank age.

Underground Storage Tanks Today

Currently, as a UST owner/operator, as long as you are compliant with federal and state regulations, you are free to operate your UST. The problems begin when the insurance marketplace will not provide financial responsibility for your UST due to the age of your tank. You could otherwise have a compliant 30-year-old tank, but as I mentioned earlier, once your storage tank sees its 20th birthday, it starts becoming difficult and cost prohibitive to insure (financial responsibility). Without the proper insurance for your tank, you are not compliant with federal and state regulations. There are no regulations pertaining to tank life and/or age, but there are financial responsibility requirements. In the insurance marketplace, any tank over 20 years old is red flagged. Experts estimate the average cost of cleaning up a leaking UST to be around $130,000 but costs can run well over one million dollars, especially if groundwater has been affected or third parties have been impacted. So, what must you know and do as an owner/operator of a UST?

Three Tasks for Tank Owners

- As soon as your UST is installed you must have a tank life cycle plan in place. Start setting money aside for the eventual removal and replacement of it. The average tank pull typically ranges from eight to fifteen thousand dollars, barring the tank has not leaked. Insurance coverage for a UST pull is scarce. Ideally you would be replacing the tank 20–25 years after the date of installation. If you did not do this, you need to play catch up and start planning as soon as possible. That day will come, and being prepared will save you time, money, and frustration.

- Ask questions and start viewing your insurance purchasing process as a relationship-building experience. Find a financially sound insurer who can provide broad coverage to meet your needs and build a strong relationship with them so that you can count on them being there for you if/when you ever need them. If you are able to obtain coverage for pulling your tank, even better!

- Understand that if you are purchasing a UST insurance policy that these policies are generally only intended to cover the structural integrity of the storage tank. They do not necessarily cover loading and unloading. Check and make sure that it does before you purchase it. Also, there is significantly broader coverage available which is extremely affordable. In addition to covering your UST it also covers third party clean up, bodily injury, and property damage, first party clean up, and typically also includes legal defense coverage. This coverage is known by a number of different names, but I will refer to it as Site Pollution Coverage. Site pollution coverage also allows you to more cost effectively insure older tanks. If you find yourself sitting on an older tank, site pollution coverage might be a great short term solution for your to evidence financial responsibility. It is also a great option if you are risk averse and prefer broader insurance coverage over self insurance.

As a tank owner, first and foremost, you need to understand that all storage tanks leak, it's only a matter of time. The insurance industry views storage tanks as "ticking time bombs." Once you understand that your storage tank has a shelf life you can proceed with taking the appropriate steps to manage your risk involved with owning/operating it. For more information about how to better operate and insure your storage tank, reach out to your Woodruff Sawyer Account Team or directly to one of our Environmental Specialists. Sources: https://www.epa.gov/ust http://plia.wa.gov/ www.landauinc.com

Table of Contents