Blog

How to Manage Exposures When Commercializing a Life Sciences Product

Camellia Baker

Camellia Baker

Nov 16, 2023

Nov 16, 2023

This article focuses on the key exposures life sciences companies face when commercializing, as well as insurance coverages that mitigate risk, avoid gaps, and reduce costs.

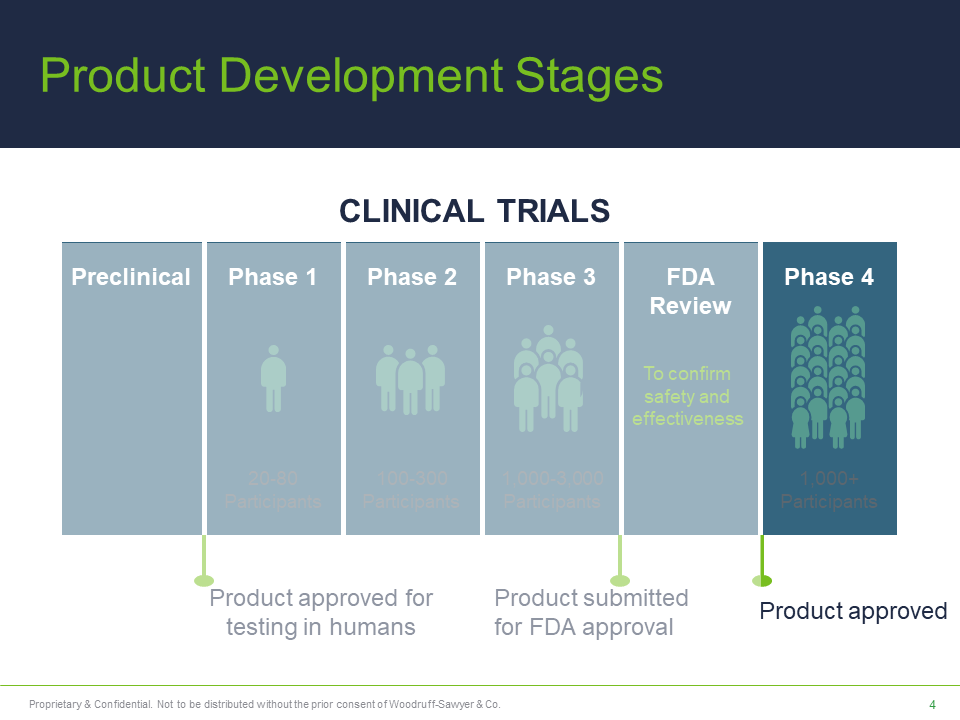

The road to commercializing a life sciences product is a long one, spanning years to perform research, develop the product, conduct clinical trials and testing, and receive approval from the Food and Drug Administration (FDA).

Commercialization, also known as Phase 4, happens after a pharmaceutical or medical device receives FDA approval. As life sciences companies stand on the precipice of commercializing their new product, it’s important to become familiar with property and casualty insurance considerations. To protect years of hard work and the profitability of your product, companies must understand the risks at the commercialization stage, review insurance coverages, and amend coverage as needed.

In this article, we focus on the key exposures life sciences companies face as they prepare to commercialize their products. We will discuss which insurance coverages to review to mitigate risk, avoid gaps, and reduce costs.

|

|

Commercialization Phase Coverages: People

Commercializing a product often means taking on additional staff to perform functions like marketing, sales, and supply chain management. This will likely require additional coverage or amendments to existing coverage.

Workers’ Compensation

Workers’ compensation insurance is statutory coverage placed to cover employees who sustain an illness or injury from a work-related cause. It also covers work-related bodily injury or disease, other than liability imposed on the insured by workers compensation laws.

When going commercial, it’s important to:

- Use the correct classification.

- Cap executive officer payroll as allowed per state, if applicable.

- Secure coverage in monopolistic states (North Dakota, Ohio, Washington, and Wyoming), which is required in these states, provided new employees reside in those states.

Employee Benefits

As companies bring on new employees to support the product commercialization phase, employee benefits like life and health insurance, retirement benefits, and others help attract quality candidates.

Business Travel and Accident Insurance

Commercialization may require the new sales force to sell the product across the country. This increases a company’s exposure to liability for death or serious injury that happens while an employee travels on behalf of the company. Business travel and accident insurance covers these types of events.

Companies may also need foreign medical coverage if employees travel outside of the country as well as coverage for dependents if they travel with the employee for work.

Commercialization Phase Insurance: Property (Assets)

Property insurance policies to cover direct physical damage to tangible property in which you have an insurable interest, including property at third-party locations. In addition to assets, business interruption is important as it covers loss of income arising from physical damage to the premises by a covered loss that causes a slowdown or suspension of operations.

Multiple coverage types exist to protect property (assets). A broker can help determine which coverages will be needed for the commercialization phase of life sciences product development.

Working with your broker, companies should:

- Review the statement of property values for potential changes.

- Review the business income worksheet and the limits listed therein. Companies may need to make changes as they shift their focus from research and development (R&D) to turning a profit and continue R&D coverage should this exposure continue after commercialization.

- Review contingent business interruption (CBI) exposures and discuss potential supply chain vulnerabilities. Oftentimes, life sciences companies outsource their product manufacturing, making them reliant on a third party to sell their product. CBI coverage is vital if the third party suffers direct damage to its property and if the third party closes, even temporarily, financially impacting the life sciences company.

- Tip: Be prepared to answer the following questions, which your broker will ask to find the appropriate coverage:

- Are raw materials used to make the product readily available?

- Does the raw-materials supplier or manufacturer source its product from one entity or are other options available?

- Is the manufacturing process relatively easy, or is it time-consuming and/or complex?

- What is the third party’s business contingency plan?

- How long will it take the third party to return to business following a closure?

- Does the company have an alternate facility to take over the work and mitigate disruptions?

- Tip: Be prepared to answer the following questions, which your broker will ask to find the appropriate coverage:

- Examine supply chain changes that will result from commercialization and reviewing contracts.

- Tip: Creating a supply-chain map can help pinpoint locations where property is housed, like raw materials storage, manufacturing facilities, or distribution centers—all of which should be evaluated for property values.

- Discuss which transportation carrier(s) will be used and the level of service they will provide (e.g., FedEx Custom Critical or other white-glove services).

- Think through potential product damage from sensitivities to temperature or vibration.

- Consider a cargo stock throughput policy to cover goods throughout the supply chain. Property programs exclude natural catastrophe exposures like damage from earthquakes, wind, or flooding. A policy can provide limited coverage.

Commercialization Phase Coverages: Liabilities

Types of casualty coverages that apply to the commercialization phase include:

- Commercial general liability

- Product liability insurance

- Errors and omissions

- Cyber insurance

- Product recall insurance

Commercial General Liability and Product Liability

In the commercialization phase, companies will have a higher risk profile compared to the R&D and clinical trial phases. Instead of basing liability coverage on square feet, lab payroll, or clinical trial participant count, it will now be based on estimated annual sales. It’s important to talk with your broker to understand how and when insurance rates will change.

To get the right level of coverage, companies will want to share with their broker whether clinical trials will continue or if they are planning trials for new products.

Errors & Omissions

Companies should also talk with their broker to assess the risk level of sales demonstrations of their new life sciences product. This will help determine whether errors & omissions insurance is needed.

Tip: To lower the risk of errors and omissions liabilities, ensure salespeople receive proper training on the new product and how to sell it.

Cyber Insurance

Companies will also want to review their level of exposure to cyberattacks. If the company is manufacturing the product, considerations should also include cyber exposures related to the manufacturing process and business income. Cyber insurance can help cover losses related to data recovery and business interruptions.

Product Recall Insurance

Companies should develop a recall plan, should something go wrong with the product. Product recall insurance can provide protection in situations like these.

Auto and Umbrella Insurance

If a company plans to have field sales representatives, it will also have more vehicles on the road. Umbrella coverage sits in excess of auto coverage, so increasing umbrella limits can help provide sufficient coverage.

To determine the right limit, a broker can perform a benchmarking limits review. A broker can also talk through best practices for monitoring employees driving their own vehicles and/or implementing a fleet safety program for drivers of company-owned vehicles.

Tip: Review umbrella limits annually and adjust them as needed.

International Insurance

If a life sciences company plans to sell or distribute the product internationally, it should confirm that its policies provide worldwide coverage.

If a company has sales offices overseas, the insurance broker should conduct an international compliance check to ensure policies meet all local coverage requirements.

An increase in overseas travel may necessitate a business travel and accident policy. If one is already in place, confirm it includes worldwide coverage. If business travel includes visits to high-risk countries, consider a kidnap & ransom policy.

Ensure Sufficient Insurance Coverage for the Commercialization Phase

The following tips are also important to keep in mind during the commercialization phase:

- Review manufacturing and other supply-chain contracts with a broker to ensure coverage complies with the company’s insurance requirements, and appropriate risk transfer is in place.

- Start discussions with a broker early, ideally six to nine months prior to commercialization.

- Develop an insurance budget to accommodate anticipated changes. Keep in mind the rating basis and the valuation of the product will change upon entering the commercialization phase, which will affect premiums.

- Review current coverage lines to determine if the policies include the appropriate scope and limits of coverage.

- Consider trade credit insurance if you’re selling to a relatively small number of customers to protect accounts receivable.

Work closely with an insurance broker who specializes in life science companies to understand your liabilities in each phase of the development and commercialization process. As your company progresses and your goals change, you will likely need to adjust your policies and take risk mitigation actions to ensure your company is fully protected, wherever you’re doing business.

Author

Table of Contents